Updated 16 Apr 2026 • 10 mins read

GigaOm Cloud FinOps Radar v5 report

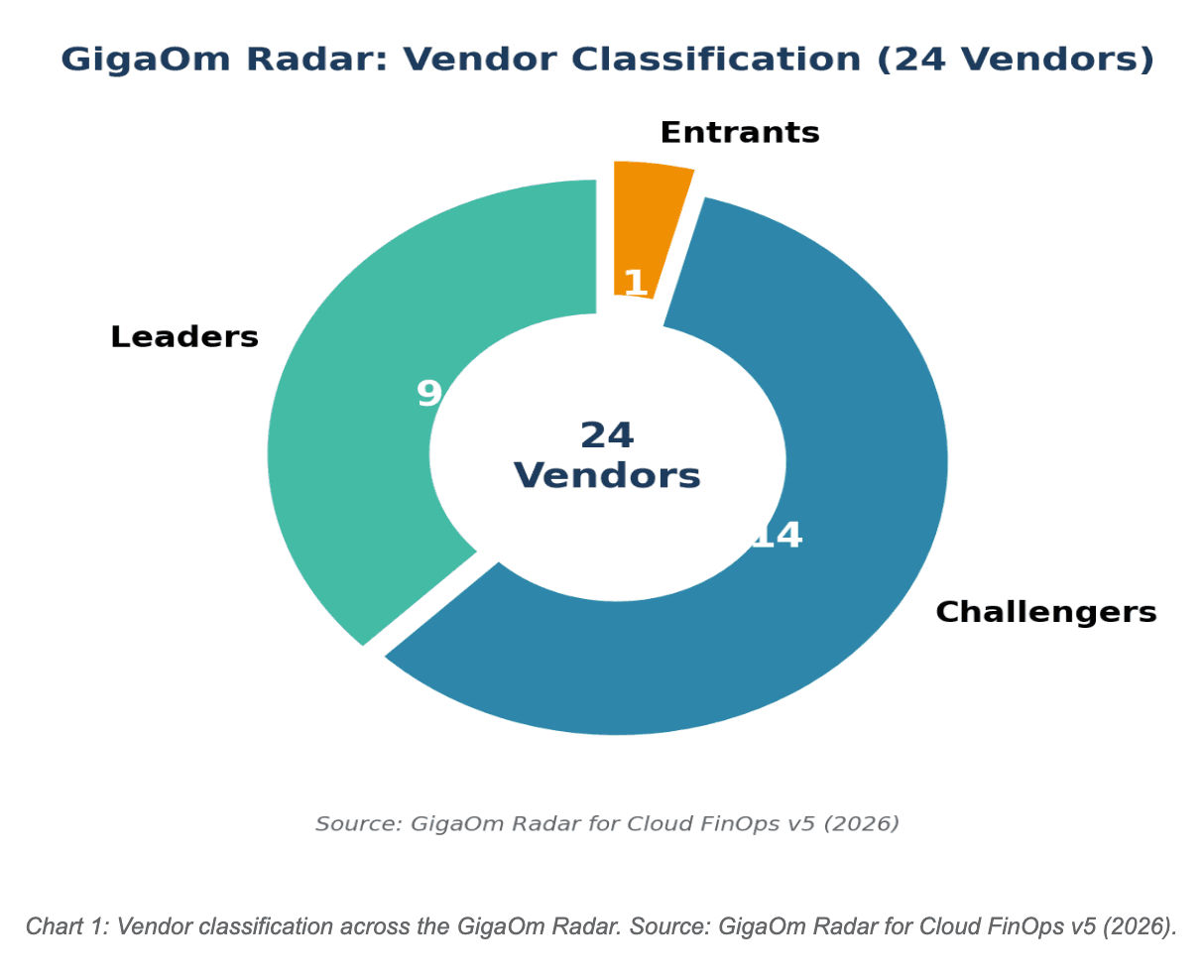

The GigaOm Radar for Cloud FinOps v5 evaluates 24 vendors across key features, emerging capabilities, and business criteria. Nine earn Leader status, with CloudBolt, Flexera, Kion, and UnityOne AI named Outperformers. The market is shifting from reactive cost reporting toward AI-driven optimization, unit economics, and platform convergence across cloud, SaaS, and AI spend. FOCUS standardization and sustainability tracking are accelerating.

Let us be honest with you. The GigaOm Radar for Cloud FinOps v5 is a fantastic report. It is also nearly 60 pages long. That is a lot of reading for anyone who is not a full-time analyst, and most of us have dashboards to watch, budgets to defend, and at least three Slack channels demanding attention at any given moment.

So we read it for you. Cover to cover. Every vendor profile. Every scoring table. Every footnote.

This blog is designed to give you everything you need to understand the full GigaOm Radar report without having to carve out half a day to read it yourself. We have distilled the key findings, mapped out the vendor landscape, highlighted what matters most for FinOps practitioners, and added our own perspective from the engineering trenches at Opslyft.

Where to find the original report: The full GigaOm Radar for Cloud FinOps v5 was authored by Dana Hernandez (Subject Matter Expert) and published by GigaOm in 2026. It evaluates 24 cloud FinOps vendors across key features, emerging capabilities, and business criteria. You can access it through GigaOm's research portal at gigaom.com.

Why it matters: If your organization is evaluating FinOps tools, planning a vendor switch, or simply trying to understand where the market is headed, this is the most comprehensive independent benchmark available right now. Our summary saves you 55 pages of effort while preserving the insights that actually drive decisions.

What Exactly Is the GigaOm Radar Report?

The GigaOm Radar is a technology-focused evaluation framework. It plots vendor solutions across concentric rings, with vendors closer to the center judged as having the most complete solutions. Each vendor is assessed on two axes: Maturity versus Innovation, and Feature Play versus Platform Play.

What makes this report different from a typical analyst comparison is its depth. Every vendor is scored across 8 key features, 8 emerging features, and 6 business criteria. Key features and business criteria carry the highest weight in determining radar positioning, while emerging features carry a lower weight but signal where the market is heading.

One important note: the Radar is purely technology-focused. Market share, brand recognition, customer count, and vendor revenue do not factor into the scoring. A smaller vendor with exceptional technology can outrank a household name. As engineers, we appreciate that kind of objectivity. The code does not care about your marketing budget.

The 2026 Cloud FinOps Vendor Landscape at a Glance

This year's report evaluates 24 vendors. That is a significant number, reflecting both the maturity and the fragmentation of the cloud FinOps market. Let us start with how they are classified.

Nine vendors earned Leader status, fourteen are classified as Challengers, and one is an Entrant. Among the Leaders, four are designated as Outperformers, meaning they are projected to make the most significant forward movement over the next 12 to 18 months.

Leaders, Challengers, and Outperformers

| Vendor | Classification | Movement | Quadrant |

|---|---|---|---|

| CloudBolt | Leader | Outperformer | Innovation / Platform Play |

| Flexera | Leader | Outperformer | Maturity / Platform Play |

| Kion | Leader | Outperformer | Innovation / Platform Play |

| UnityOne AI | Leader | Outperformer | Innovation / Platform Play |

| Exivity | Leader | Fast Mover | Innovation / Feature Play |

| Harness | Leader | Fast Mover | Innovation / Platform Play |

| HPE Morpheus | Leader | Fast Mover | Innovation / Platform Play |

| IBM | Leader | Fast Mover | Maturity / Platform Play |

| Ternary | Leader | Fast Mover | Innovation / Platform Play |

Where the Vendors Actually Sit: Quadrant Analysis

The radar's two-axis system creates four quadrants, and understanding which quadrant a vendor falls into tells you a lot about its approach and DNA.

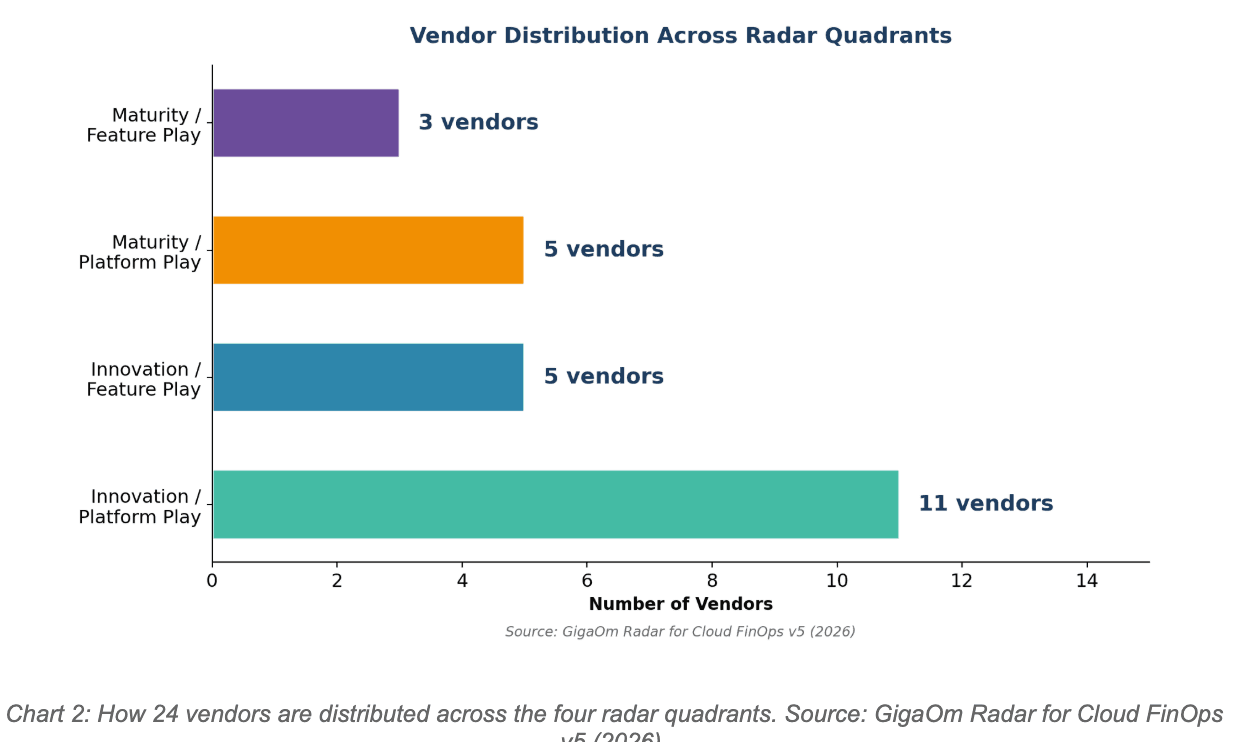

The Innovation / Platform Play quadrant is by far the most crowded with 11 vendors. This makes sense. The FinOps market is still relatively young and evolving rapidly. Many vendors are building broad platform capabilities that extend beyond just cost visibility into areas like AI cost management, automated remediation, and lifecycle orchestration.

Vendors in the Maturity half of the chart have had platforms in the FinOps market for a long time. Several are key members of the FinOps Foundation. They continue to be strong players but tend to add new functionality at a slower pace or through acquisitions.

The Innovation / Feature Play quadrant houses vendors with strong but narrower capabilities. Some focus specifically on billing accuracy, others on short-term optimization, and some specialize in intelligent forecasting. These vendors often get paired with a broader solution to provide depth in a particular area.

From the engineering side: the fact that 11 out of 24 vendors sit in the Innovation / Platform Play quadrant tells us something important. The market is consolidating around platforms, not point solutions. If you are evaluating tools today, make sure you are picking something that will grow with you, not something you will need to replace in 18 months.

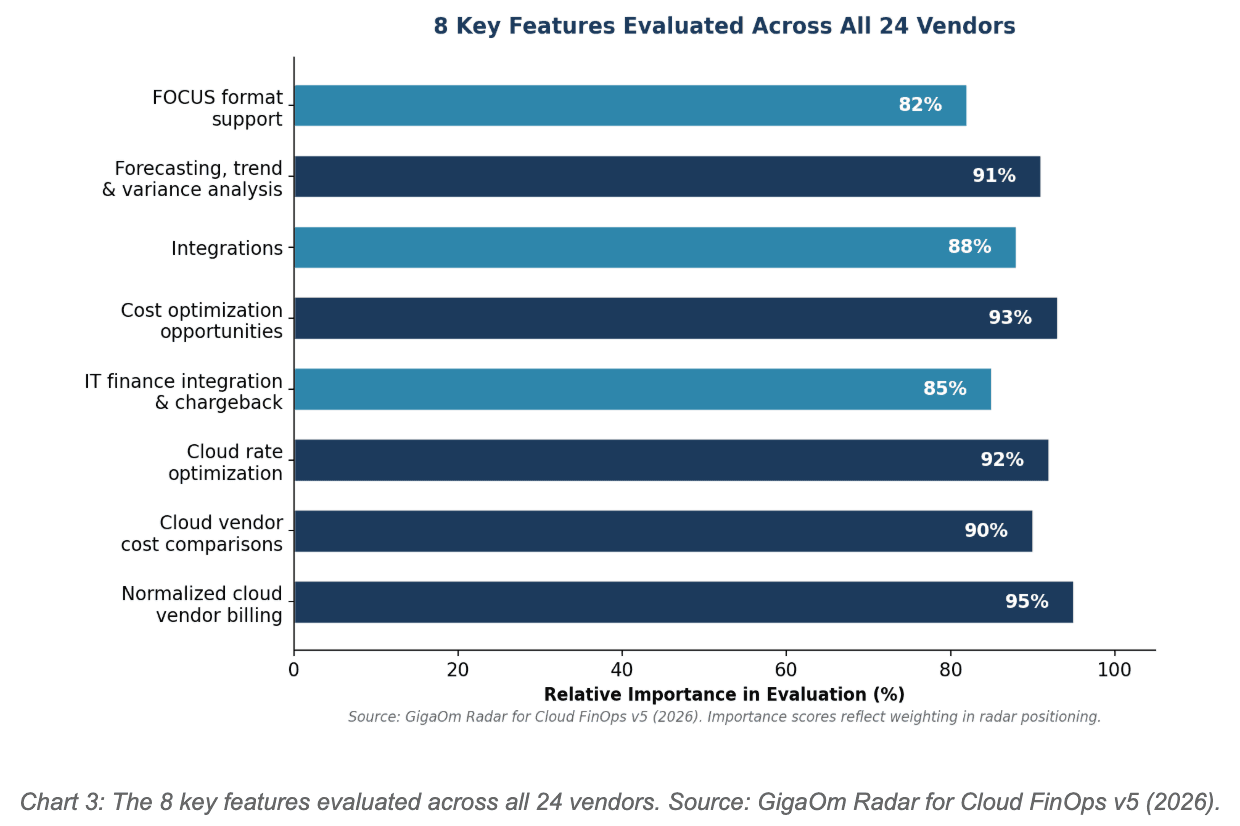

The 8 Key Features That Separate Good from Great

Every vendor in the report meets a baseline of table stakes capabilities: dynamic pricing extraction from multiple clouds, budget alerts, security controls, shared cost management, cost allocation and showback, and tagging. Those are entry tickets. What actually differentiates vendors are the 8 key features GigaOm evaluates.

Normalized cloud vendor billing is the foundation of everything. In a multicloud world, you need to hide the complexity of different billing formats and show directly comparable costs. Without this, every decision requires manual translation. Cloud rate optimization and the identification of cost optimization opportunities have the highest practical impact for most organizations because they directly translate into savings.

FOCUS format support is worth paying attention to. The FinOps Foundation's FOCUS specification standardizes cost and usage data across providers. It is still evolving, but vendors with native FOCUS support (like CloudBolt, which built its entire architecture on FOCUS) are better positioned for the future than those retrofitting support after the fact.

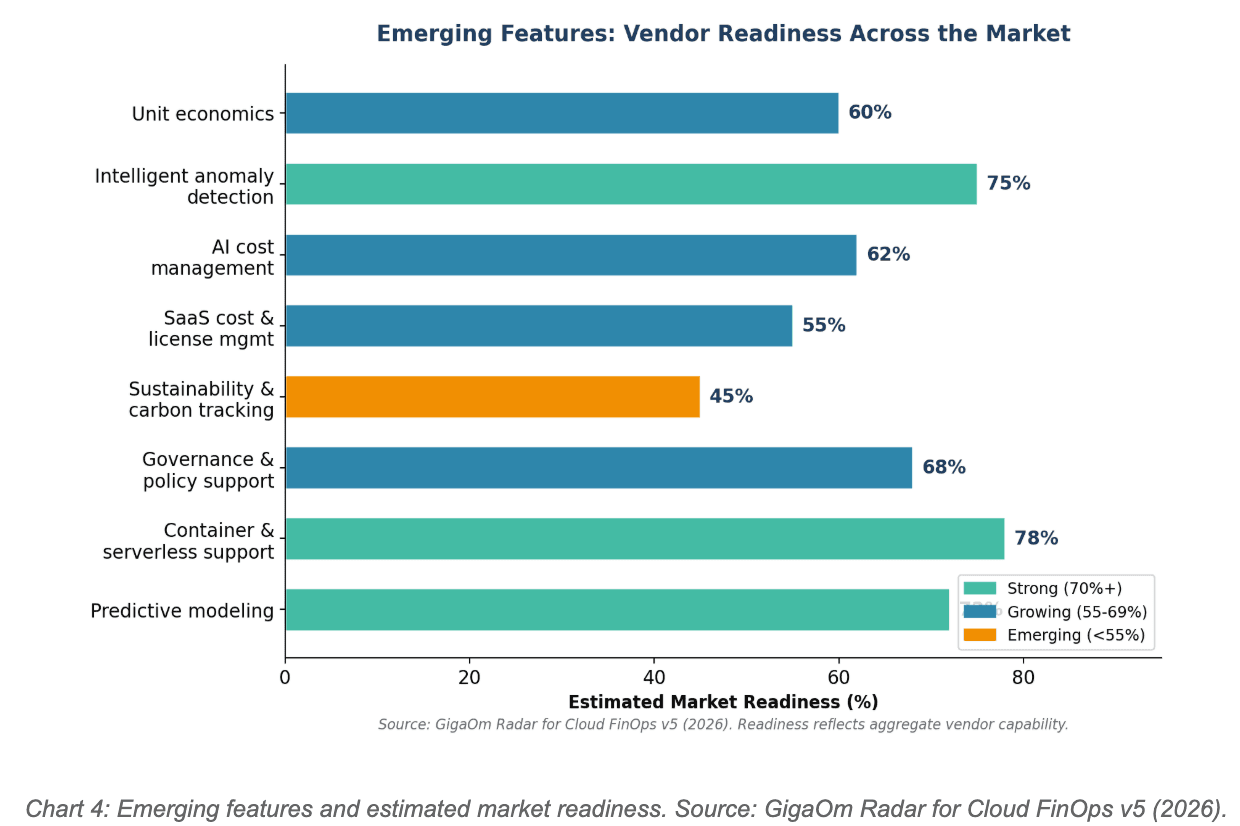

8 Emerging Features: Where the Market Is Headed

Emerging features do not carry as much weight in the radar scoring today, but they signal where vendor investment and customer demand are heading over the next 12 to 18 months.

Container and serverless support, predictive modeling, and intelligent anomaly detection are the most mature emerging capabilities. These make sense because Kubernetes adoption is now mainstream, and AI-driven anomaly detection is a natural evolution of traditional threshold-based alerting.

Sustainability and carbon footprint tracking is still the least mature capability, with only about 45% market readiness. Most vendors offer limited carbon reporting or depend on exported Excel files. Given the growing regulatory pressure around sustainability, this gap will not last long.

AI cost management is the feature we at Opslyft are watching most closely. As organizations scale GenAI workloads, understanding and controlling AI-specific costs is becoming critical. The vendors that crack this problem well will have a significant competitive advantage.

The SQL query running your monthly FinOps report costs pennies. The LLM inference endpoint your team launched last Tuesday might cost more than your entire Q1 compute budget. AI cost management is not a nice-to-have anymore. It is a survival skill.

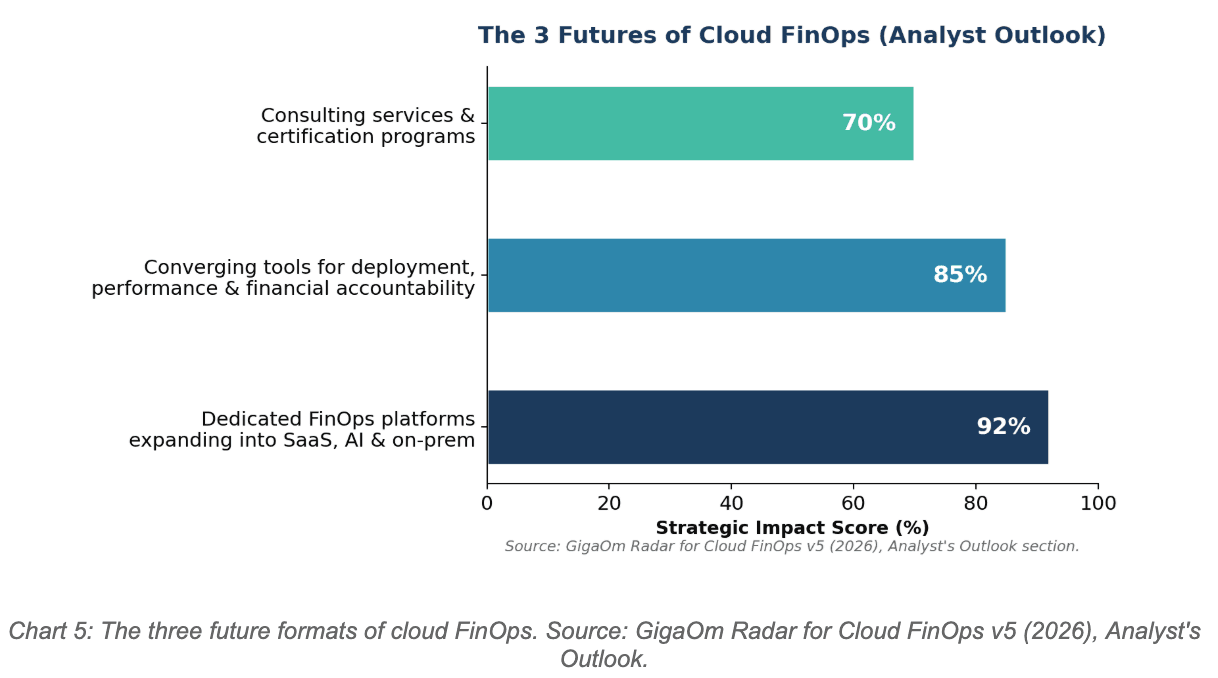

The Analyst's View: Three Futures of Cloud FinOps

The report's analyst outlook section lays out a compelling vision for where FinOps is heading. According to GigaOm, the future of cloud FinOps will play out in three distinct formats.

The first and most impactful trend is dedicated FinOps platforms expanding beyond cloud into SaaS, AI, and on-premises spend. This is the convergence play. The tools that win will be the ones that can give you a unified view across your entire technology estate, not just your AWS or Azure bill.

The second trend is the merging of deployment management, performance optimization, and financial accountability into single workflows. Think of it as the end of context-switching: one tool to deploy, monitor, and manage the cost of a workload.

The third trend is the growing role of consulting services and training certifications. The FinOps Foundation is leading this effort, and the report notes that almost all 24 vendors have Foundation memberships, with 10 holding premier status and 14 having certified platforms.

At Opslyft, we believe the first trend is the most transformative. Organizations that are still managing cloud costs, SaaS costs, and AI costs in separate spreadsheets are fighting a losing battle against complexity. Unified platforms are not a luxury anymore. They are a necessity.

Quick Reference: Key Takeaways at a Glance

| Dimension | Key Finding |

|---|---|

| Total vendors evaluated | 24 (9 Leaders, 14 Challengers, 1 Entrant) |

| Top Outperformers | CloudBolt, Flexera, Kion, UnityOne AI |

| Most crowded quadrant | Innovation / Platform Play (11 vendors) reflecting the young, fast-evolving market |

| Most critical key feature | Normalized cloud vendor billing (foundation for every other capability) |

| Most impactful emerging feature | AI cost management and intelligent anomaly detection |

| Least mature emerging feature | Sustainability and carbon footprint tracking (still early stage) |

| Market direction | Moving from reactive reporting to proactive AI-driven optimization with unit economics |

| FinOps Foundation standard | FOCUS format adoption accelerating; SCOPES framework extending into SaaS and PaaS |

Conclusion

The GigaOm Radar for Cloud FinOps v5 paints a picture of a market that is maturing rapidly but still full of movement. Nine Leaders, four Outperformers, and a strong cluster of Innovation-focused platform vendors tell us that the FinOps tooling landscape is consolidating around broader, AI-powered platforms that go well beyond basic cost visibility.

For organizations evaluating vendors today, the report makes a few things clear. First, look beyond just billing accuracy. The table stakes are table stakes for a reason. What will differentiate your FinOps program is unit economics, AI cost management, automated remediation, and native support for the FOCUS standard. Second, pay attention to the emerging features. Sustainability tracking, SaaS license management, and predictive modeling may feel optional today, but they will be core requirements within 18 months. Third, choose a platform that matches your complexity. If you are running a hybrid, multi-cloud environment with growing AI workloads, you need a Platform Play vendor, not a Feature Play specialist.

At Opslyft, we believe the best FinOps tool is the one that gives your engineering, finance, and leadership teams a single, shared view of reality. The vendors that deliver that clarity will win. The ones that don't will become features inside someone else's platform.

The FinOps market is no longer about whether you need a tool. It is about whether the tool you pick can keep up with you.

FAQs

It is a comprehensive evaluation of 24 FinOps vendors based on features, innovation, and business criteria, highlighting market leaders and trends.

CloudBolt, Flexera, Kion, and UnityOne AI stand out as top outperformers with strong innovation and platform capabilities.

AI workloads can significantly increase cloud expenses, making cost visibility and optimization essential for maintaining financial control.

FOCUS is an open specification that standardizes cloud billing data, enabling better cost comparison and improved financial decision-making.